How it works

The math, shown — not a black-box “AI answer.”

blankit doesn’t guess the right renewal number with a model. It walks the same actuarial sequence a credentialled consultant would — and shows every step in the report you send back to the carrier.

The workflow

Three steps, ten minutes.

Step 1

Upload

Drop in the renewal PDF.

Any carrier format — Sun Life, Manulife, Canada Life, GreenShield, RBC, Equitable, Co-operators, regional carriers. blankit extracts the renewal letter, experience pages, and rate calculations into a structured document. Prefer not to upload? Forward the renewal to your firm’s email-in address or drop it in a connected cloud folder — it starts the same analysis.

Step 2

Analyze

Run the actuarial engine.

Every benefit line (EHC, Dental, Life, ADD, STD, LTD) goes through the same five-step calculation. The result is a defensible counter-number, line-by-line, with carrier-comparable units.

Step 3

Report

Send the firm-branded PDF back.

The output is a renewal challenge report — your firm’s logo, your firm’s colors, your firm’s tone — with executive summary, line-by-line math, and a recommendation the carrier can't hand-wave away.

The methodology, in full

Eight steps. One defensible number per line.

Every step below runs for every health-line benefit on the renewal. The same logic appears as a footnote on the report PDF — so when the underwriter pushes back, the answer is already on the page.

- 01

Strip large claimants, re-add pool charge

Individual claimants above $25,000 are removed from paid claims and replaced with a standard pool-charge PMPM. This isolates the experience the group is actually responsible for — and exposes how much of the “premium” is really pooled risk the carrier never had to fund.

- 02

Remove the pooling charge from gross premium

The carrier's pooling charge is removed from gross premium to reveal net premium — what was actually available to cover group claims. This is the denominator the carrier doesn't want shown.

- 03

Add IBNR to incurred claims

Incurred-but-not-reported claims are loaded onto paid claims. For EHC and Dental the IBNR figure is never guessed — it comes from the carrier’s own disclosure, your booklet library, or a value you enter, so the number on the page is one the carrier can’t wave away. This is the numerator that gets the loss ratio right.

- 04

Compute the real net loss ratio

Incurred claims ÷ net premium. Materially higher than the carrier-quoted gross loss ratio, because the denominator dropped and the numerator rose. This is the negotiating number.

- 05

Trend from experience midpoint to renewal midpoint

When the renewal discloses its trend assumption, blankit uses the carrier’s own figure — there’s nothing to argue about. When it doesn’t, line-specific factors calibrated against settled Canadian renewals project the experience period forward to the policy period being priced.

- 06

Credibility-blend with the carrier’s manual rate

Square-root rule (Limited Fluctuation Credibility) blends the trended group experience with the carrier’s implied manual rate. Larger groups carry more weight; smaller groups borrow more from the manual.

- 07

Gross up by the carrier’s own target loss ratio

Health and dental are grossed up by the carrier’s target loss ratio — the figure you set per client from the carrier’s renewal, your booklet library, or Salesforce. Holding the carrier to their own pricing target, not a guessed benchmark, is what makes the methodology aggressive and defensible.

- 08

Cap at the carrier proposal

blankit will never recommend paying more than the carrier asked for. The "fair" premium is the lower of the calculated value and the carrier proposal.

Provincial mechanics

The Québec adjustments most national tools quietly skip.

Group plans for Québec employers cover less than equivalent plans in other provinces — because the provincial system already covers part of the disability stack. blankit applies these offsets automatically so the trended PMPM lands at the right number, not the carrier’s default-Ontario assumption.

STD · QPIP offset

0.85×Québec Parental Insurance Plan absorbs the parental-leave portion of short-term disability. blankit drops the STD trended PMPM by 15% for QC groups before credibility blending.

LTD · CNESST offset

0.90×The Commission des normes, de l’équité, de la santé et de la sécurité du travail covers a slice of long-term disability claims in Québec. blankit drops the LTD trended PMPM by 10% for QC groups.

In the product

Where the methodology lives.

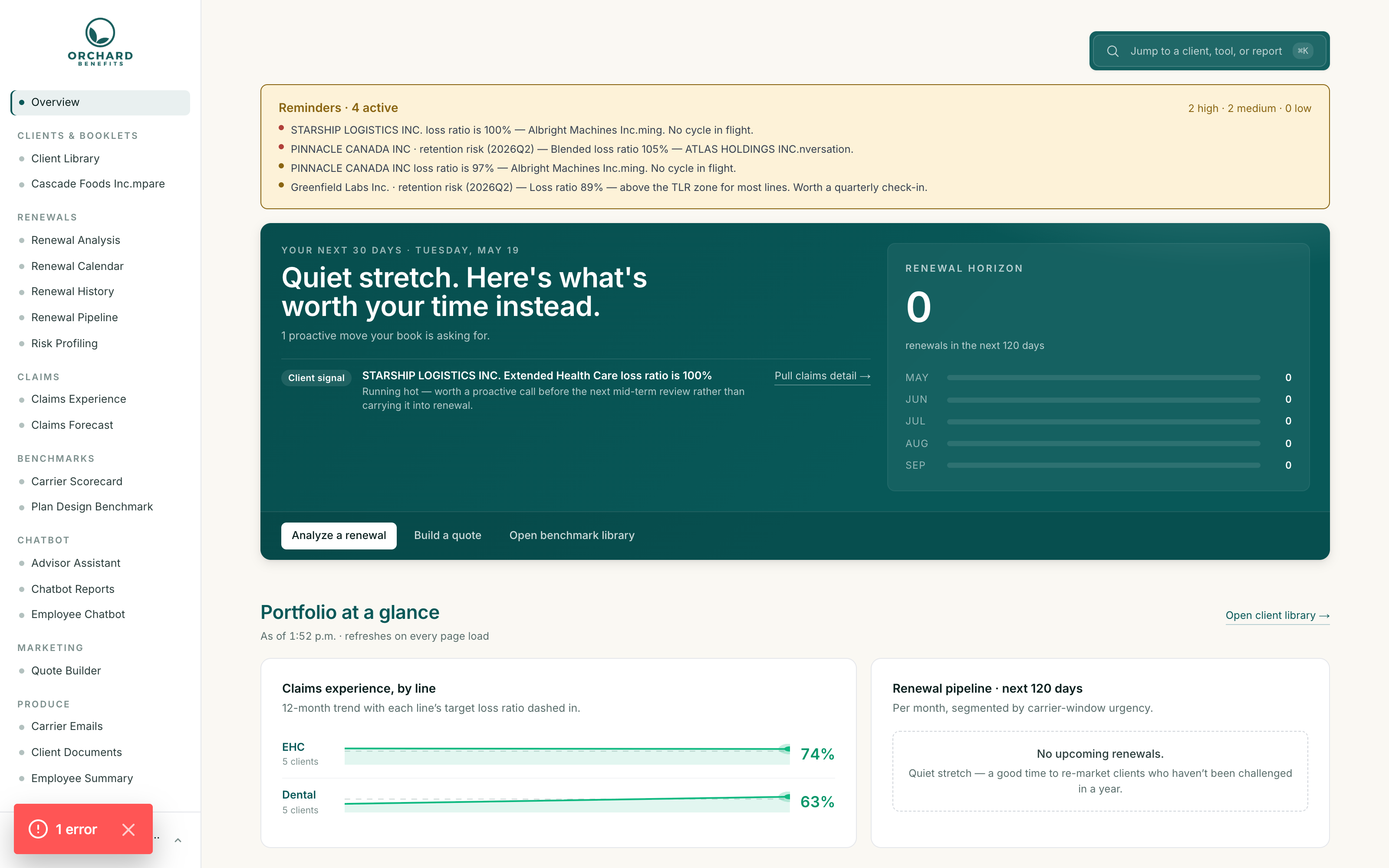

Practice dashboard

Renewal pipeline, client library, claims experience, and benchmarks in one surface.

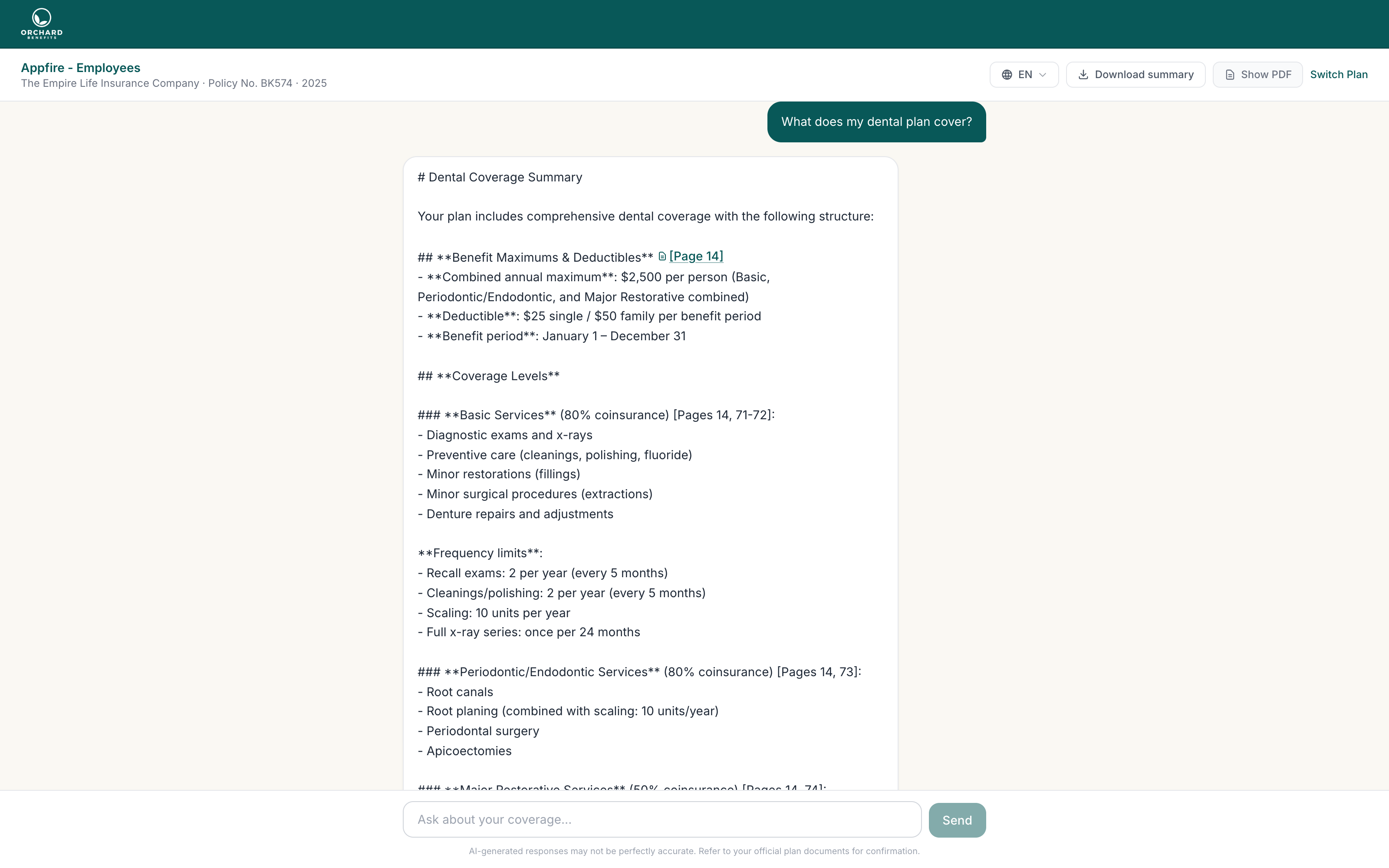

Employee benefits chatbot

Booklet-grounded Q&A for plan members, white-labelled to the employer.

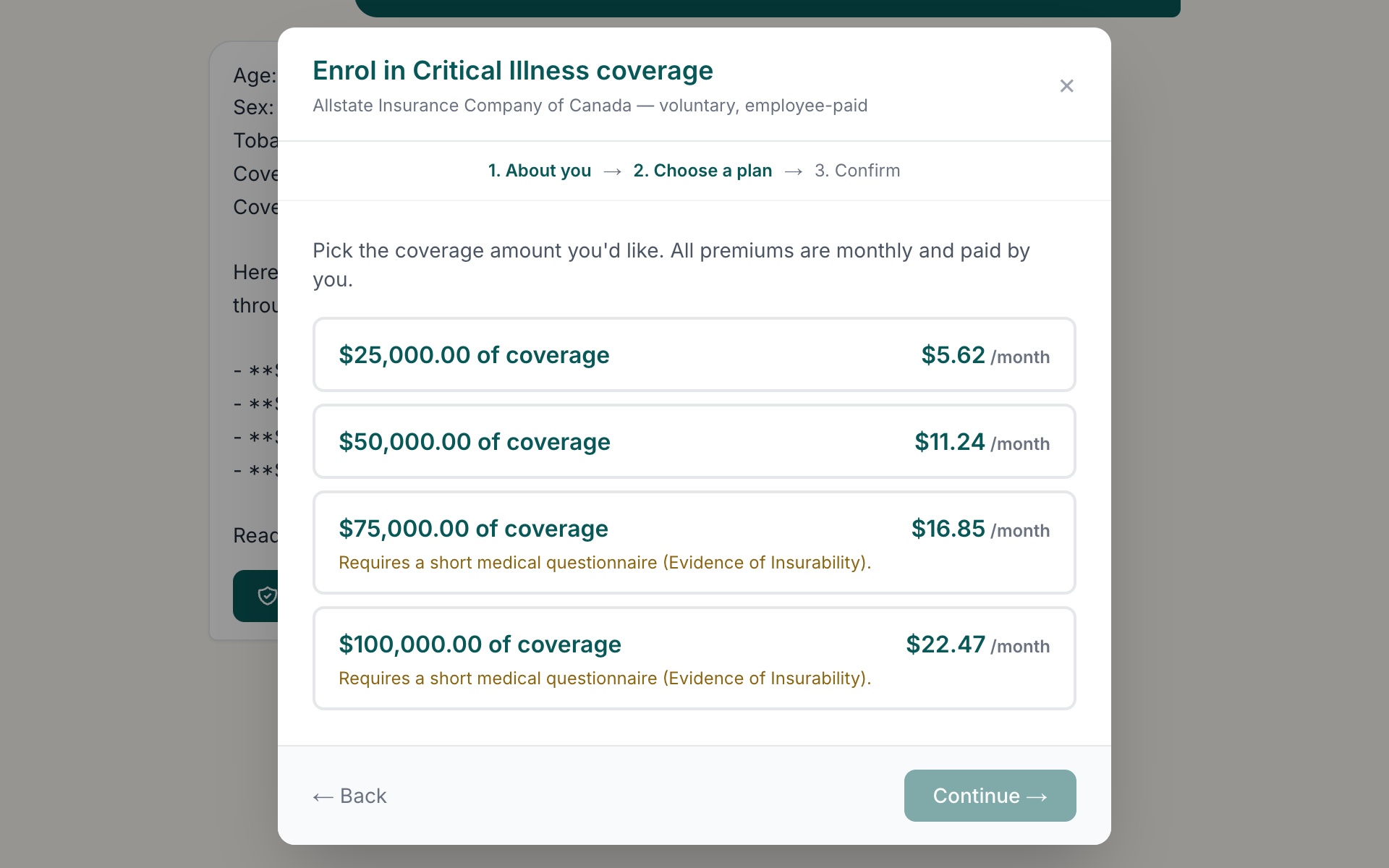

Critical illness enrolment

Plan members buy supplemental CI coverage in minutes, with carrier-bound rates.

Support access

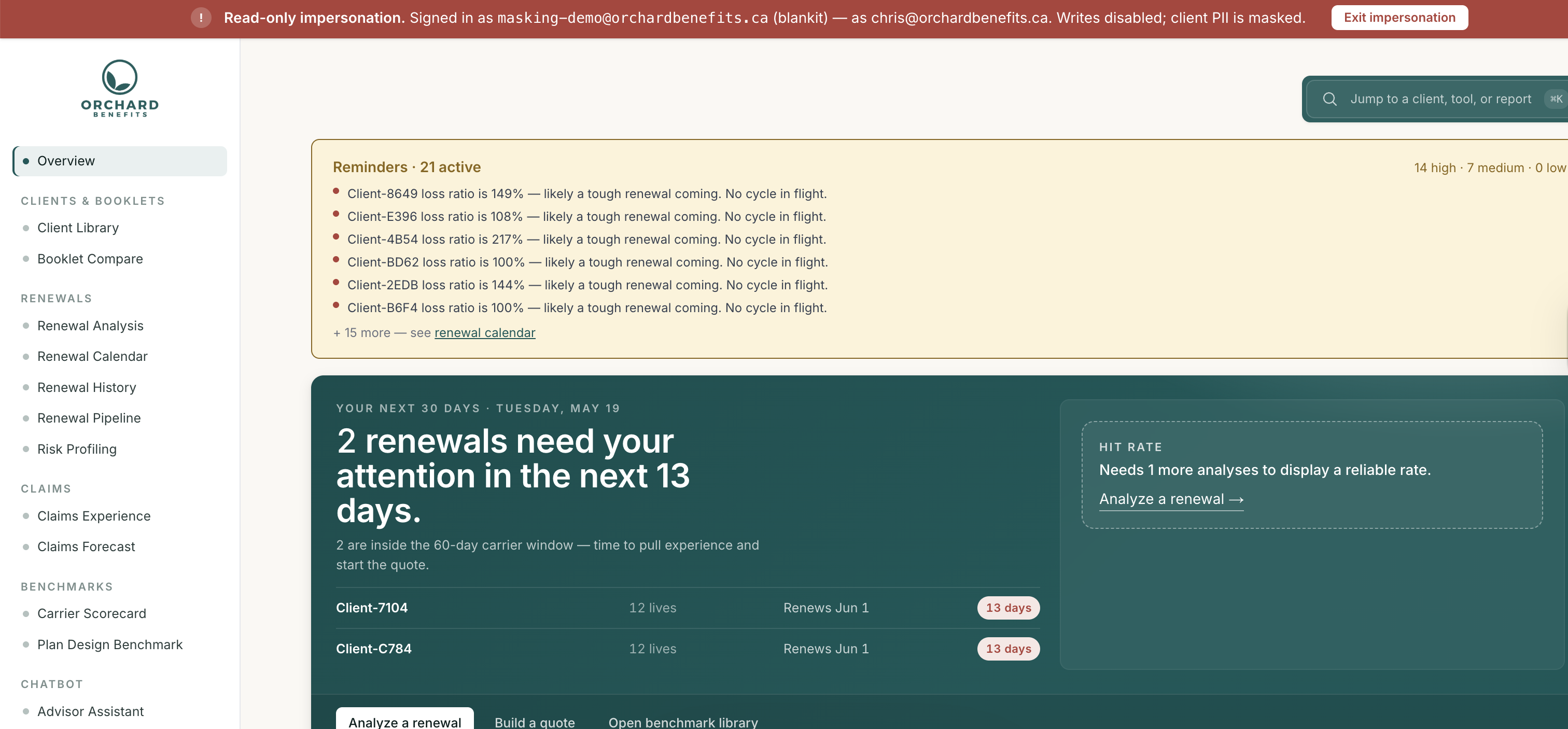

What support sees when we're inside your firm — and what stays hidden.

Once a tenant is provisioned, the engineer who built blankit can't open it the way a senior advisor at your firm can. The day-to-day product is firmId-scoped at the database layer: cross-firm reads aren't a permission to grant, they aren't a code path.

The exception is support. When a problem inside your data needs an engineer, the platform admin can start a read-only impersonation session that lasts thirty minutes. The session is two things at once: gated against writes at the edge middleware, and rewritten at the data layer.

Stays visible

- Carriers

- Dollars and loss ratios

- Dates and headcount

- Benefit lines and provinces

- The shape of every page

Replaced or redacted

- Client and contact names →

Client-XXXX - Emails and phone numbers

- Document titles and filenames

- Policy and group numbers

- Free-text blobs (notes, JSON)

Pseudonyms are deterministic — the same client gets the same code across pages, sessions, and refreshes. That way a support conversation can reference a specific case without exposing identity. Every session start and end is recorded in the audit log under the operator's identity.

Pull a real renewal and watch the methodology run.

Book a demo and we’ll run your most recent carrier renewal through the engine on screen. You leave with the counter-number and a firm-branded challenge PDF.